When you deposit tokens into a DeFi liquidity pool, you’re not just earning fees-you’re also taking on a hidden risk called impermanent loss. It’s not a glitch. It’s not a hack. It’s math. And if you don’t understand it before you deposit, you could lose money-even when the price of your assets goes up.

What Exactly Is Impermanent Loss?

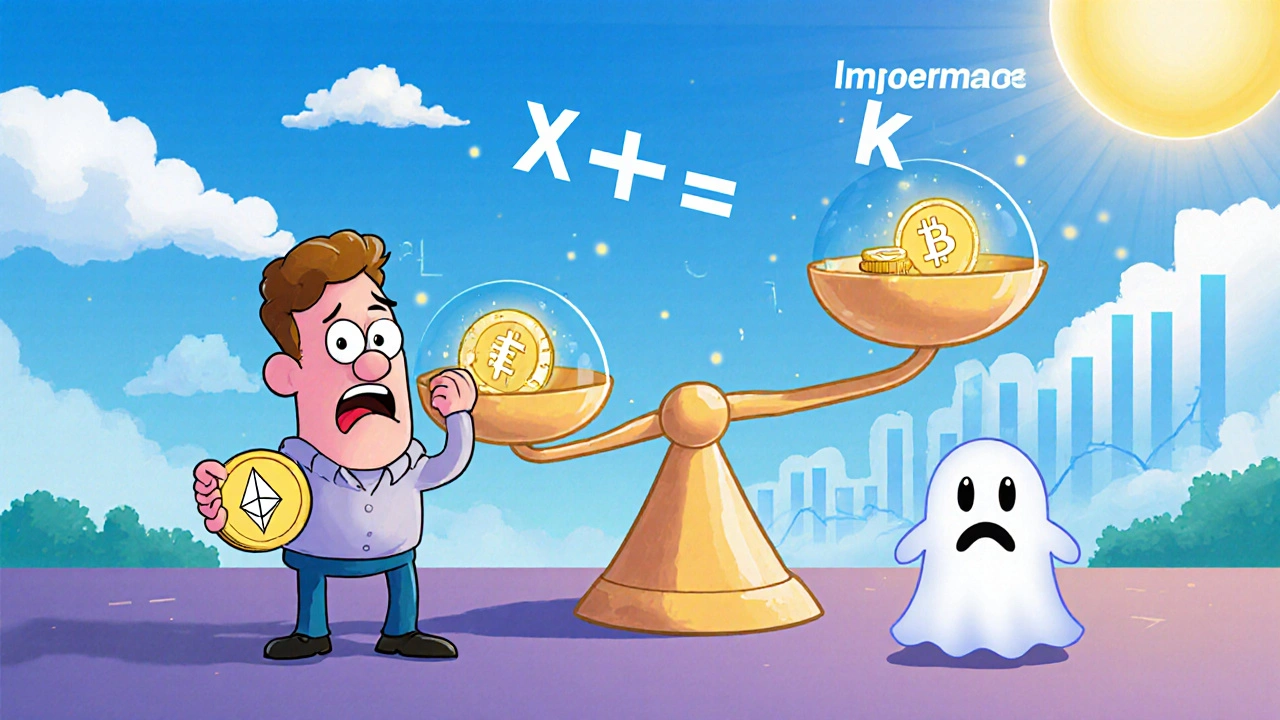

Impermanent loss happens when the price of one asset in a liquidity pool changes compared to the other. You’re not losing coins. You’re losing value relative to just holding those coins in your wallet. Here’s how it works: You put $1,000 worth of ETH and $1,000 worth of DAI into a Uniswap V2 pool. That’s a 50/50 split. The pool uses a formula called x * y = k to keep trading smooth. If ETH’s price doubles from $100 to $200, traders will buy ETH from the pool using DAI until the pool’s price matches the market. The pool automatically rebalances: you end up with less ETH and more DAI than you started with. When you withdraw, your total value might be $2,828, but if you’d just held your original 10 ETH and 1,000 DAI, you’d have $3,000. That $172 gap? That’s impermanent loss. The word “impermanent” is misleading. If ETH drops back to $100, the loss disappears. But if you withdraw while ETH is at $200? The loss becomes permanent. You didn’t lose tokens-you lost opportunity cost.Why Does It Happen?

Automated Market Makers (AMMs) like Uniswap, Curve, and Balancer don’t use order books. They use math to set prices. The constant product formula forces the pool to sell low and buy high. When ETH rises, the pool sells ETH to buy DAI. When ETH falls, it sells DAI to buy ETH. That’s how it keeps prices aligned with the market. But here’s the catch: you’re not the one setting the price. The algorithm is. And it doesn’t care if you’re long-term holding ETH. It just rebalances to match the external market. That’s why you end up with a different mix of tokens than you started with. The bigger the price swing, the bigger the loss. A 2x price change? That’s about 5.7% loss. A 4x change? Nearly 20%. A 5x? Over 25%. And it doesn’t matter if the price goes up or down. Only the ratio matters.Not All Pools Are Equal

Some pools are designed to avoid this. Stablecoin pools like USDC/USDT barely experience impermanent loss-even if one coin moves 10%, the loss is under 0.5%. That’s because their values are meant to stay close. But if you’re putting ETH and SOL into a pool? That’s a different story. Those assets move independently. One can surge while the other stalls. That’s when impermanent loss spikes. Uniswap V2 is the most vulnerable. It forces a 50/50 split and uses the basic formula. Curve Finance is built for stablecoins. Balancer lets you use custom ratios like 80/20, which reduces exposure. But the real game-changer is Uniswap V3.

Uniswap V3: The Smart Fix

Uniswap V3 lets you pick a price range. Instead of spreading your $1,000 across every possible price, you lock it between, say, $180 and $220 for ETH. If ETH stays in that range, your capital is fully active-and you earn more fees. If ETH moves outside, your position becomes inactive, but your loss is capped. A 2x price move in V2? 5.7% loss. Same move in V3 with a smart range? As low as 3.2%. But if you set your range too wide-like $50 to $500-you’re back to V2-level risk. Too narrow? You get out of the pool too easily. It’s not passive. You need to adjust. Tools like Gamma Strategies automate this. They monitor price movements and shift your V3 positions to stay in the sweet spot. That cuts impermanent loss by over 40% on average.Fees Can Save You

Here’s the silver lining: trading fees offset a lot of this loss. In high-volume pools like ETH/USDC, fees can cover 60-80% of the impermanent loss. One user on Reddit lost 14.8% on a UNI/ETH pool when ETH doubled-but earned $427 in fees over 92 days. That turned a net loss into a 3.5% gain. The key question isn’t “Will I have impermanent loss?” It’s “Will my fees beat it?” Check the APY on DeFiLlama. If a pool offers 15% APY and your estimated impermanent loss is 8%, you’re still ahead. But if the APY is 3% and the loss is 10%? You’re losing money.

Common Mistakes to Avoid

Most people lose money not because they don’t understand the math-they just skip the basics.- Depositing into volatile pairs without checking the calculator: 28% of beginners do this. Don’t be one of them.

- Withdrawing during a price swing: 37% of people panic and pull out when the loss hits. That turns impermanent into permanent.

- Ignoring fees: 63% of new LPs don’t factor them in. They see a 7% loss and think they’re down-when fees might’ve made them up 5%.

- Using V2 for volatile pairs: V3 exists for a reason. If you’re not using it, you’re overpaying in risk.

How to Protect Yourself

You don’t need to be a math genius. Just follow these steps:- Use an impermanent loss calculator before depositing. Sites like ilcalculator.com let you plug in asset pairs and price changes. It takes 2 minutes.

- Stick to stablecoin pairs if you want near-zero loss. USDC/USDT, DAI/USDC-they’re safe.

- Use Uniswap V3 with tight ranges for volatile assets. Don’t guess. Use tools like Gamma or DeFi Saver to auto-manage.

- Compare APY to estimated loss. If fees won’t cover the math, walk away.

- Never withdraw during a big price move. Wait. Let the market settle. The loss might reverse.

The Bigger Picture

As of late 2025, over 70% of new DeFi users say impermanent loss is their top concern before depositing. Institutions are already adapting-63% of institutional DeFi players use concentrated liquidity (V3) to reduce exposure. New AMM designs are coming. Research from UC Berkeley suggests future pools could cut impermanent loss by 65-80%. But until then, the rules haven’t changed: know your math, use the right tools, and don’t treat liquidity provision like a free lunch. It’s not about avoiding risk. It’s about managing it. The best liquidity providers aren’t the ones who never lose-they’re the ones who know exactly how much they’ll lose, and still come out ahead.Is impermanent loss real or just theoretical?

It’s real. You can see it in your wallet. If you deposited $2,000 worth of ETH and USDC and now your position is worth $1,900 even though ETH’s price went up, that’s impermanent loss. It’s not a bug-it’s how AMMs work. The only thing "impermanent" about it is that it can reverse if prices return to their original ratio. But if you withdraw while prices are off, the loss becomes permanent.

Does impermanent loss happen with stablecoin pools?

Almost never. Pools like USDC/USDT or DAI/USDC are designed to keep prices stable. Even if one coin moves 10%, the impermanent loss is under 0.5%. That’s why stablecoin liquidity provision is the safest entry point for beginners. The fees still add up, and the risk is minimal.

Can I avoid impermanent loss entirely?

Not completely, but you can reduce it dramatically. Use Uniswap V3 with narrow price ranges, stick to stablecoin pairs, or use automated tools like Gamma Strategies that adjust your positions. If you’re only providing liquidity to assets that move together (like different stablecoins or wrapped tokens), your exposure is nearly zero. But if you’re putting ETH and a new memecoin into a pool? You’re signing up for big risk.

Do trading fees always cover impermanent loss?

No. In low-volume pools, fees might be 1-2% APY while impermanent loss is 8-10%. That’s a net loss. But in high-volume pools like ETH/USDC or WBTC/ETH, fees often cover 60-80% of the loss. Always check the 7-day fee yield on DeFiLlama before depositing. If fees are below 5% APY and you’re in a volatile pair, you’re probably better off just holding.

Why is Uniswap V3 better than V2 for avoiding impermanent loss?

Uniswap V2 spreads your capital across all possible prices. V3 lets you concentrate it where you think the price will stay. If ETH is trading at $2,000, you can lock your liquidity between $1,800 and $2,200. If it stays there, your capital earns fees 10x more efficiently than V2. If ETH moves outside, you’re out of the pool-but you didn’t lose as much. V3 reduces impermanent loss by 30-50% when used correctly. But it requires active management. V2 is passive. V3 is smarter-but you have to work for it.

Should I stop providing liquidity because of impermanent loss?

No-if you manage it right. Impermanent loss isn’t a reason to avoid DeFi. It’s a reason to be smarter. Many experienced users earn 10-20% APY net after fees and loss by sticking to stablecoin pools or using V3 with automated tools. The people who lose money are the ones who deposit blindly into volatile pairs and ignore the math. Know your risk. Use the tools. Track your fees. You can make money-even with impermanent loss.